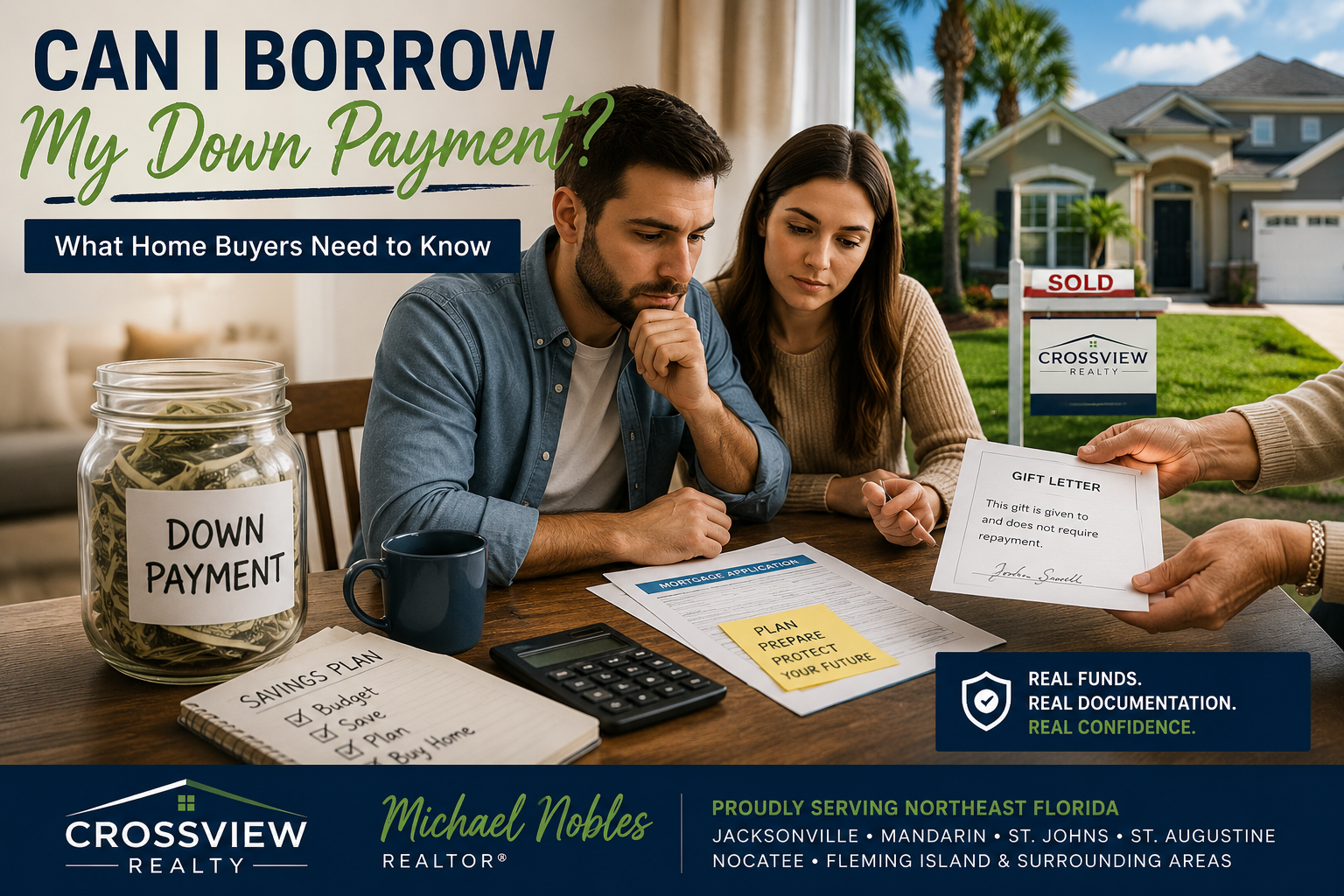

Can I Borrow My Down Payment?

Can I borrow my down payment when buying a home?

The short answer is usually no. Most lenders want your down payment to come from your own funds or from an approved gift source. The reason is simple: the down payment is intended to show that you have a financial stake in the property and to reduce the amount of money being financed.

Why Do Lenders Care Where the Down Payment Comes From?

When a lender reviews your mortgage application, they look closely at your income, credit score, assets, and liabilities. One of the most important calculations they make is your debt-to-income ratio, which compares how much you owe each month to how much income you earn.

If you borrow money from another source to make your down payment, you are increasing your debt load. That additional debt can affect your ability to qualify for a mortgage or may result in a higher interest rate.

The lender wants to be confident that you can comfortably afford the mortgage payment without taking on additional debt just to get into the home.

What Sources of Down Payment Funds Are Allowed?

In most cases, lenders prefer that your down payment comes from:

Savings accounts

Checking accounts

Retirement accounts (when permitted)

Investment accounts

Approved gift funds from family members

If a family member, such as a parent, provides money for your down payment, the lender will typically require documentation showing that the funds are a gift and do not need to be repaid.

This usually involves a gift letter and documentation showing where the funds came from.

What Happens If Money Suddenly Appears in My Bank Account?

One of the most common questions I hear from buyers is why the lender asks so many questions about their bank statements.

The answer is that lenders are required to verify the source of your funds. Large deposits that recently appeared in your account will often be questioned. The lender wants to know where the money came from and whether it represents additional debt that could affect your ability to repay the mortgage.

Because of this, it is important to keep good records and be prepared to explain any unusual deposits.

My Advice to Home Buyers

My recommendation is to start saving for your down payment as early as possible. Most buyers will need anywhere from 3% to 20% down depending on the type of loan and the property being purchased. Investment properties often require larger down payments than primary residences.

If you have cash that you plan to use for a future purchase, deposit it into your bank account well before applying for a mortgage. This helps establish a clear paper trail showing that the funds belong to you.

Most importantly, never misrepresent where your money came from. Be honest with your lender and provide the documentation they request. These guidelines are designed to protect both you and the lender and help ensure a smooth transaction.

Final Thoughts

Buying a home is one of the largest financial decisions most people will ever make. Understanding where your down payment can come from can save you time, stress, and potential delays during the loan approval process.

As a real estate agent with CrossView Realty serving Jacksonville, Mandarin, St. Johns, St. Augustine, Nocatee, Fleming Island, and the surrounding Northeast Florida communities, I work with buyers every day who have questions about financing, down payments, and loan requirements. The more prepared you are before applying for a mortgage, the smoother your home-buying experience will be.

Ready to Buy a Home?

If you have questions about down payments, financing options, or buying a home in Northeast Florida, I'd be happy to help. Contact Michael Nobles with CrossView Realty to discuss your options and connect with trusted local lenders who can guide you through the mortgage process.

Michael Nobles

CrossView Realty

www.michaelnoblesrealtor.com